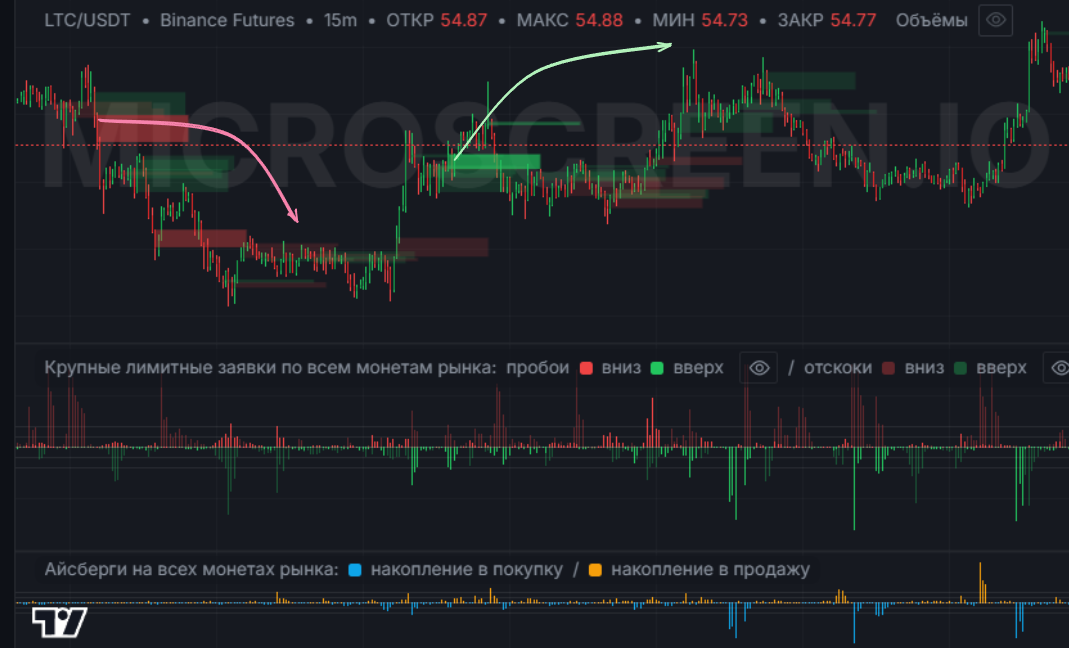

Local accumulation before move

Buy-side liquidity clusters appearing before directional expansion.

Used as a pre-entry confirmation layer to filter weak breakouts and low-quality impulses.

I research order flow signals, build the tools to test them, and look for a prop firm or fund where this work runs on real capital.

Systematic backtesting has been formalized on self-collected Binance Futures microstructure data since November 2024. The window is constrained by data depth because the order book and trade-flow aggregates are collected with my own infrastructure, which also means the research stack is fully under my control.

Live deployment started in 2026, about one week before the Iran war. The strategy showed positive results in its first week of live trading, then ran into a sharp drawdown during the Iran war shock in early 2026, a regime where the underlying microstructure signals stopped behaving normally. Risk management forced a stop.

The response was to simplify, not to optimize harder. Fewer rules, tighter regime filters, more explicit market-wide pressure checks, and a cleaner view of where the signal degrades under stress. The revised version went live again on April 29, 2026.

These are not marketing visuals. They are working screens used to make market behavior observable, comparable, and testable.

Buy-side liquidity clusters appearing before directional expansion.

Used as a pre-entry confirmation layer to filter weak breakouts and low-quality impulses.

Synchronized buy-side or sell-side activity across many instruments at once.

Used to distinguish local noise from broad market participation and to tighten regime filtering.

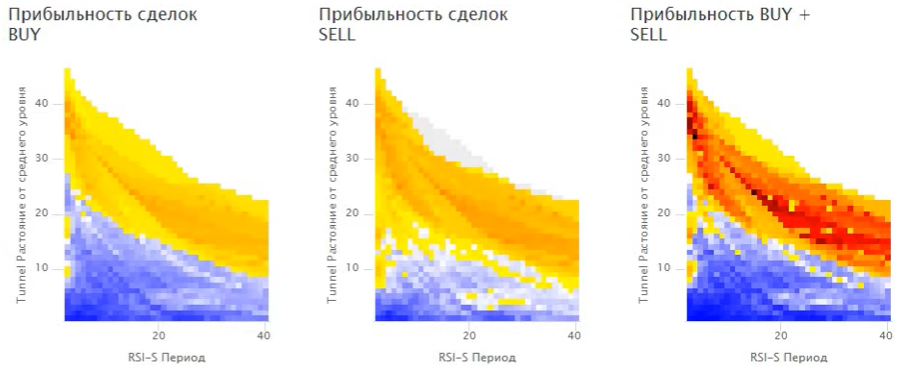

Signal quality is judged by stable regions, not by a single best point.

Used to reject fragile optimizations and keep the strategy inside robust parameter neighborhoods.

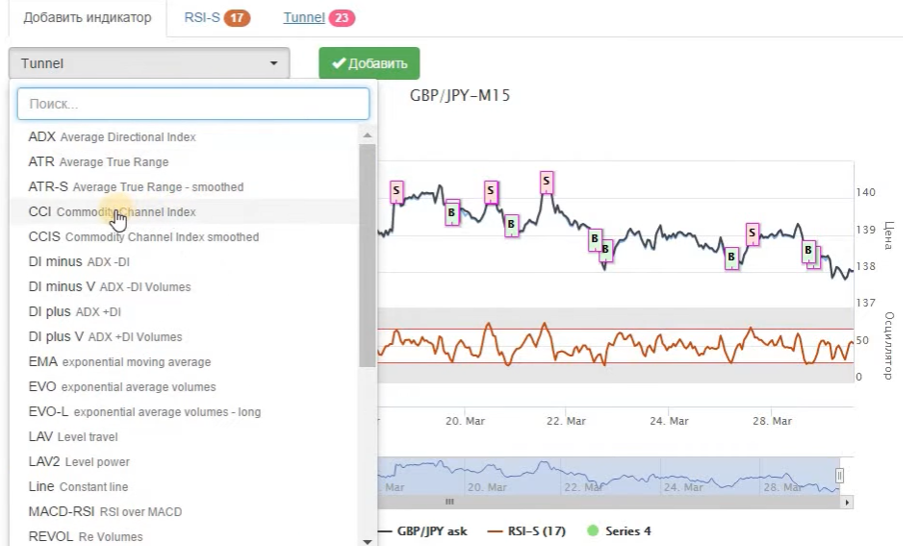

Internal interfaces for visual construction and fast testing of trading hypotheses.

Built to compress the path from market anomaly to testable hypothesis in hours rather than days.

Performance is always read together with drawdown structure, fill assumptions, and regime sensitivity.

The objective is not a beautiful backtest. The objective is a strategy that survives realistic execution and stress periods.

The edge is not only the signal - it is the loop: observation, hypothesis, validation, rejection, and revision under real execution constraints.

Annualized Sharpe ~5, systematic backtest since November 2025, Binance Futures, conservative fill assumptions.

Backtest period: November 2025 - April 2026 on self-collected Binance Futures data. Live deployment started: April 2026. Results below reflect systematic backtest with conservative execution assumptions.

Data is self-collected, which constrains the window but gives full pipeline control. Access to deeper historical data inside a fund would immediately expand the testing horizon.

Figures represent one primary strategy. Multiple additional strategies were tested and most were discarded during validation.

Conservative execution assumptions: 0.1% round-trip fee plus 0.6% slippage for trades executed with market orders. The slippage assumption is based on real trading across different coins with average trade size up to 50,000 USDT.

The bottleneck in quant research is rarely ideas. It is the distance between observation and validation. Every tool here is designed to compress that distance.

I build the internal systems required to observe microstructure, structure hypotheses, and move from raw signals to repeatable evaluation.

A serious trading team does not benefit from isolated notebooks or one-off charts. It benefits from a research system that can be extended, debugged, and used repeatedly under pressure.

The value is not a dashboard. The value is faster rejection of weak ideas, faster confirmation of strong ones, and better understanding of when a signal stops being real.

I want to do the same work inside a stronger environment: better capital, better data, better infrastructure, and a team where research quality actually matters.

What I bring: microstructure signal research, internal tooling that compresses the research loop, and strategies built with execution constraints from day one.

Compensation model: base plus meaningful profit participation. Details in direct conversation.

Full-time or long-term contract. Remote is fine. I research microstructure signals, build internal tooling, and contribute strategies that can survive real execution constraints.

Internal systems for backtesting, signal monitoring, execution-aware analytics, and market structure observability. Best fit for teams that already trade and need more research throughput.

Short-term engagement for research pipeline acceleration, backtesting architecture, data collection, or microstructure monitoring systems.

I'm not interested in selling signals or running a fund. I want to be inside a team that takes the research seriously.

The underlying approach is shaped less by ideology and more by repeated contact with execution reality.

Price patterns often reflect attention and psychology. Microstructure reveals actual interaction: liquidity, aggressive flow, iceberg behavior, and coordinated activity.

Complex rule stacks usually overfit noise. Simple signals with positive expectancy and explicit filters tend to hold up longer.

A strategy that works in stable, rotational markets can fail badly in fast directional or shock regimes. Regime classification is central, not optional.

The practical answer is not perfect prediction. It is resilience through allocation logic, pressure checks, and rules that degrade gracefully.

Liquidity, slippage, and market impact define real scale. Many attractive signals disappear once size becomes nontrivial.

Far liquidity is often noise or bluff. The information that matters most tends to live near the actual execution zone.

I'm a systems engineer who spent the last 10 years learning how markets actually behave and building tools to act on that understanding.

Before that, I spent 20+ years building products and infrastructure from zero across fintech, SaaS, and AI-adjacent systems.

Based in Moscow, GMT+3. Working remotely across time zones.

I want to bring microstructure research and tooling into a team - and absorb what serious practitioners know about sentiment, on-chain flow, and ML-driven signal enhancement that I have not yet built myself.

I prefer direct conversations over formal process. If this resonates, reach out on Telegram.

If you run a prop desk, crypto fund, or trading operation and you're looking for someone who researches microstructure signals and builds the tools to act on them, I'm interested.

No pitch decks. No NDA on first contact. Just a direct conversation.